According to Latvia’s State Revenue Service, Bolt now controls approximately 98% of the app-based taxi and ride-sharing market in Riga, a near-complete erasure of every independent operator that existed before the platform arrived and priced aggressively enough to make competition unsustainable.

The licensed taxi industry in Latvia has publicly described this as a de-facto monopoly. Bolt’s commission in the Latvian market has been reported at over 30%, a figure that becomes defensible for a platform once competition disappears, because drivers have nowhere else to go.

The arithmetic that independent drivers need to face

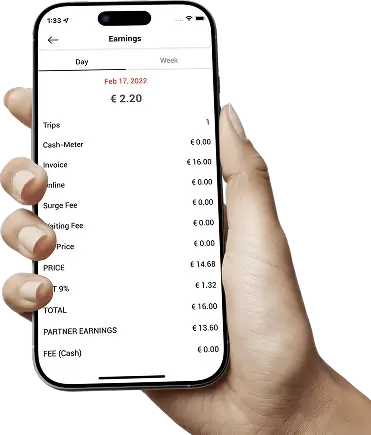

A driver completing 40 trips a week at an average fare of €90 generates €3,600 in gross revenue. At 30% commission, €1,080 goes to the platform before fuel, insurance, maintenance, or the driver's own time are accounted for. At a fairer commission rate of 15%, that same driver keeps €540 more every single week, which compounds to over €28,000 a year from commission alone.

The platform knows this arithmetic as well as the driver does. It also knows that once competition is gone, the commission rate is entirely its decision to make.

Why isolation is the real vulnerability

The independent drivers who survived platform consolidation in markets across Europe share a common characteristic. They were working with others when the pressure arrived. They had built client relationships that ran through their own reputation rather than a platform’s algorithm. They had professional connections with other drivers that allowed them to cover overflow, share trips, and collectively serve corporate clients that no single driver could handle alone.

A driver who depends entirely on one platform for their income has exactly one point of failure. A driver who has direct client relationships, a network of trusted colleagues, and multiple income streams has considerably more resilience when a platform decides to change its terms.

What the Netherlands is watching

Bolt and Uber’s presence in Dutch cities is growing. The market is far from 98% platform concentration, but the direction is clear and the pace is increasing. The independent operators who will still be running profitable businesses in five years are the ones building their foundations now, before the pressure makes building them harder.

The Riga situation is a straightforward lesson about what happens when a fragmented group of independent professionals fails to build the connections and infrastructure that would have made them collectively strong enough to compete.

The platform won because it was organised and the alternative was fragmented. That is the only real lesson Riga has to offer, and it is one that independent operators in every European market should be taking seriously right now.